1

2

3

4

5

6

7

8

9

10

11

12

|

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

from scipy import stats

import statsmodels.api as sm

from sklearn.model_selection import train_test_split

from sklearn.metrics import mean_squared_error

plt.style.use('fivethirtyeight')

sales = pd.read_csv('Album_sales_2.txt',sep='\t')

sales

|

|

adverts |

sales |

airplay |

attract |

| 0 |

10.256 |

330 |

43 |

10 |

| 1 |

985.685 |

120 |

28 |

7 |

| 2 |

1445.563 |

360 |

35 |

7 |

| 3 |

1188.193 |

270 |

33 |

7 |

| 4 |

574.513 |

220 |

44 |

5 |

| ... |

... |

... |

... |

... |

| 195 |

910.851 |

190 |

26 |

7 |

| 196 |

888.569 |

240 |

14 |

6 |

| 197 |

800.615 |

250 |

34 |

6 |

| 198 |

1500.000 |

230 |

11 |

8 |

| 199 |

785.694 |

110 |

20 |

9 |

- advers : 광고비

- sales: 판매량

- airplay : 음반 출시전 한 주 동안 노래들이 라디오1에 방송된 횟수

- attract : 밴드 매력(0~10)

1. EDA

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 200 entries, 0 to 199

Data columns (total 4 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 adverts 200 non-null float64

1 sales 200 non-null int64

2 airplay 200 non-null int64

3 attract 200 non-null int64

dtypes: float64(1), int64(3)

memory usage: 6.4 KB

|

adverts |

sales |

airplay |

attract |

| count |

200.000000 |

200.000000 |

200.000000 |

200.00000 |

| mean |

614.412255 |

193.200000 |

27.500000 |

6.77000 |

| std |

485.655208 |

80.698957 |

12.269585 |

1.39529 |

| min |

9.104000 |

10.000000 |

0.000000 |

1.00000 |

| 25% |

215.917750 |

137.500000 |

19.750000 |

6.00000 |

| 50% |

531.916000 |

200.000000 |

28.000000 |

7.00000 |

| 75% |

911.225500 |

250.000000 |

36.000000 |

8.00000 |

| max |

2271.860000 |

360.000000 |

63.000000 |

10.00000 |

1

2

3

4

5

|

plt.style.use('seaborn-pastel')

plt.figure(figsize=(10,10))

for i,j in enumerate(sales.columns):

plt.subplot(2,2,i+1)

sns.histplot(sales[j])

|

<seaborn.axisgrid.PairGrid at 0x1e5f655a940>

1

|

sns.heatmap(sales.corr(),annot=True,cmap='Blues')

|

<AxesSubplot:>

`시각화를 통해 보았을 때 advert가 치우쳐서 변수 변환이 필요할 수 있다는 점 빼고 큰 특징은 보이지 않는다.

상관성이 좀 있는 편인데 일단 회귀 분석을 진행하면서 결과를 살펴봐야겠다.

2. train, test로 분리 후 다중회귀분석 결과 해석

1

|

x_train, x_test, y_train, y_test = train_test_split(sales.iloc[:,[0,2,3]], sales['sales'],)

|

상수항 넣었을 때

1

|

x_data = sm.add_constant(x_train, has_constant = "add")

|

1

2

3

4

|

# const넣음

model = sm.OLS(y_train,x_data)

result = model.fit()

result.summary()

|

OLS Regression Results

| Dep. Variable: | sales | R-squared: | 0.651 |

| Model: | OLS | Adj. R-squared: | 0.644 |

| Method: | Least Squares | F-statistic: | 90.71 |

| Date: | Fri, 09 Oct 2020 | Prob (F-statistic): | 3.44e-33 |

| Time: | 14:24:41 | Log-Likelihood: | -789.91 |

| No. Observations: | 150 | AIC: | 1588. |

| Df Residuals: | 146 | BIC: | 1600. |

| Df Model: | 3 | | |

| Covariance Type: | nonrobust | | |

| coef | std err | t | P>|t| | [0.025 | 0.975] |

| const | -36.6149 | 21.619 | -1.694 | 0.092 | -79.341 | 6.111 |

| adverts | 0.0825 | 0.008 | 10.032 | 0.000 | 0.066 | 0.099 |

| airplay | 3.4240 | 0.314 | 10.897 | 0.000 | 2.803 | 4.045 |

| attract | 12.5468 | 2.997 | 4.187 | 0.000 | 6.624 | 18.470 |

| Omnibus: | 0.238 | Durbin-Watson: | 1.725 |

| Prob(Omnibus): | 0.888 | Jarque-Bera (JB): | 0.189 |

| Skew: | 0.086 | Prob(JB): | 0.910 |

| Kurtosis: | 2.972 | Cond. No. | 4.41e+03 |

1

2

|

y_pred = result.predict(ols.add_constant(x_test, has_constant = "add"))

mean_squared_error(y_pred,y_test)

|

2128.1345418881824

1

2

3

4

|

# 안 넣음

model2 = sm.OLS(y_train,x_train)

result2 = model2.fit()

result2.summary()

|

OLS Regression Results

| Dep. Variable: | sales | R-squared (uncentered): | 0.950 |

| Model: | OLS | Adj. R-squared (uncentered): | 0.949 |

| Method: | Least Squares | F-statistic: | 928.3 |

| Date: | Sun, 11 Oct 2020 | Prob (F-statistic): | 2.75e-95 |

| Time: | 23:09:26 | Log-Likelihood: | -791.37 |

| No. Observations: | 150 | AIC: | 1589. |

| Df Residuals: | 147 | BIC: | 1598. |

| Df Model: | 3 | | |

| Covariance Type: | nonrobust | | |

| coef | std err | t | P>|t| | [0.025 | 0.975] |

| adverts | 0.0797 | 0.008 | 9.830 | 0.000 | 0.064 | 0.096 |

| airplay | 3.3006 | 0.308 | 10.731 | 0.000 | 2.693 | 3.908 |

| attract | 8.1136 | 1.468 | 5.525 | 0.000 | 5.212 | 11.016 |

| Omnibus: | 0.694 | Durbin-Watson: | 1.762 |

| Prob(Omnibus): | 0.707 | Jarque-Bera (JB): | 0.587 |

| Skew: | 0.153 | Prob(JB): | 0.745 |

| Kurtosis: | 2.990 | Cond. No. | 300. |

aic는 비슷하나 R-squared 면에서 상수항이 없는게 나음

1

2

|

y_pred = result2.predict(x_test)

mean_squared_error(y_pred,y_test)

|

2093.0726936877363

1

2

|

plt.plot(y_test.values)

plt.plot(y_pred.values)

|

VIF

1

2

|

from statsmodels.stats.outliers_influence import variance_inflation_factor

[variance_inflation_factor(x_train.values,i) for i in range(3)]

|

[2.6632477766856404, 5.761240629832455, 6.855611086457372]

대체로 크게 나오는 편은 아니다.

변수가 적어 모든 변수 조합에서 Variance와 mse를 살펴 봄

1

2

3

4

5

6

|

from itertools import combinations

joint = []

for i in range(1,4):

k = combinations(x_train.columns,i)

for j in k:

joint.append(j)

|

[('adverts',),

('airplay',),

('attract',),

('adverts', 'airplay'),

('adverts', 'attract'),

('airplay', 'attract'),

('adverts', 'airplay', 'attract')]

1

2

3

4

5

6

|

stepw = []

for i in joint:

model = sm.OLS(y_train,x_train[list(i)])

result = model.fit()

y_pred = result.predict(x_test[list(i)])

stepw.append([list(i),result.aic,mean_squared_error(y_pred,y_test)])

|

1

2

3

|

stepw_frame = pd.DataFrame(stepw, columns=['Variables','AIC','MSE'])

stepw_frame.set_index('Variables',inplace=True)

stepw_frame

|

|

AIC |

MSE |

| Variables |

|

|

| [adverts] |

1832.620857 |

9775.286334 |

| [airplay] |

1716.242475 |

5246.164309 |

| [attract] |

1727.874967 |

6423.816111 |

| [adverts, airplay] |

1615.042139 |

2447.023190 |

| [adverts, attract] |

1673.510244 |

3376.763066 |

| [airplay, attract] |

1662.523096 |

4237.857648 |

| [adverts, airplay, attract] |

1588.737818 |

2093.072694 |

3개 다 선택했을 때 값이 가장 적게 나온다.

다중회귀분석의 매개변수별 신뢰구간

|

0 |

1 |

| adverts |

0.063717 |

0.095782 |

| airplay |

2.692710 |

3.908404 |

| attract |

5.211536 |

11.015580 |

3. 독립성, 정규성 가정 평가

1

2

|

# 독립성

sns.regplot(result2.fittedvalues, result2.resid, lowess=True, line_kws={'color': 'red'})

|

1

2

|

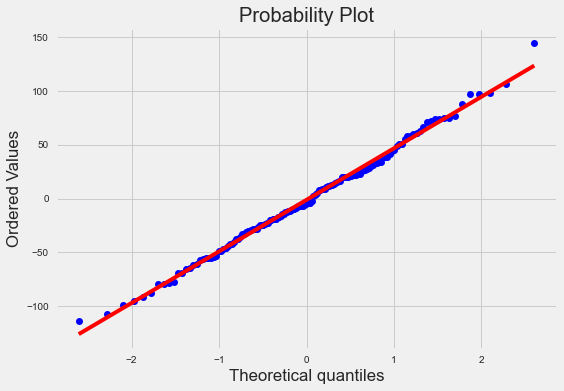

#정규성

stats.probplot(result2.resid,plot=plt);

|

1

|

stats.shapiro(result2.resid)

|

(0.9950959086418152, 0.8982971906661987)

- 독립성과 정규성을 만족하는 편이다.

- summary에서 durbin-watson 값이 1.5~2.5 안에 있어야 정상이라고 함

4. 표준화잔차, cook’s distance, DFBeta, 공분산비 보기

- 표준화잔차(standard_resid) : 잔차를 표준오차로 나눈 값

- cook’s distance : 관측치가 제거되었을 때 모수 추정값들의 (동시적) 변화량 척도

- DFBeta : 관측값이 각각의 회귀계수에 미치는 영향력을 측정

- DFFITS : 관측치가 예측값에서 보유하고 있는 영향력을 측정

1

2

3

|

infl = result2.get_influence()

sm_fr = infl.summary_frame()

sm_fr

|

|

dfb_adverts |

dfb_airplay |

dfb_attract |

cooks_d |

standard_resid |

hat_diag |

dffits_internal |

student_resid |

dffits |

| 23 |

-0.000441 |

-0.009346 |

0.000516 |

0.000159 |

-0.238252 |

0.008315 |

-0.021816 |

-0.237486 |

-0.021746 |

| 33 |

-0.005728 |

0.022027 |

-0.020366 |

0.000221 |

-0.152693 |

0.027656 |

-0.025751 |

-0.152185 |

-0.025666 |

| 117 |

-0.004076 |

0.000292 |

-0.001237 |

0.000026 |

-0.133886 |

0.004372 |

-0.008872 |

-0.133438 |

-0.008842 |

| 93 |

-0.054948 |

-0.212492 |

0.243871 |

0.020558 |

1.247608 |

0.038112 |

0.248342 |

1.249992 |

0.248816 |

| 64 |

-0.029928 |

-0.040401 |

0.068245 |

0.001846 |

0.489364 |

0.022606 |

0.074423 |

0.488095 |

0.074230 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

| 153 |

-0.050052 |

0.055071 |

-0.006892 |

0.002166 |

0.452345 |

0.030779 |

0.080610 |

0.451118 |

0.080391 |

| 130 |

0.002361 |

0.053852 |

-0.030313 |

0.001554 |

0.697670 |

0.009485 |

0.068270 |

0.696447 |

0.068151 |

| 104 |

-0.048983 |

0.167837 |

-0.092858 |

0.010958 |

0.829723 |

0.045577 |

0.181316 |

0.828839 |

0.181123 |

| 161 |

0.094157 |

0.025861 |

-0.098308 |

0.005490 |

-1.127330 |

0.012794 |

-0.128339 |

-1.128377 |

-0.128458 |

| 183 |

-0.028555 |

-0.003881 |

0.015144 |

0.000299 |

-0.089645 |

0.100417 |

-0.029951 |

-0.089342 |

-0.029850 |

1

2

3

4

5

6

7

|

album_sales_diagnostics = pd.concat([x_train,y_train],axis=1)

album_sales_diagnostics['cook'] = infl.cooks_distance[0]

album_sales_diagnostics['resid_std'] = infl.resid_studentized

album_sales_diagnostics[['dfbeta_adverts','dfbeta_airplay','dfbeta_attract']] = infl.dfbeta

album_sales_diagnostics['covariance'] = infl.cov_ratio

album_sales_diagnostics.head()

|

|

adverts |

airplay |

attract |

sales |

cook |

resid_std |

dfbeta_adverts |

dfbeta_airplay |

dfbeta_attract |

covariance |

| 23 |

656.137 |

34 |

7 |

210 |

0.000159 |

-0.238252 |

-0.000004 |

-0.002884 |

0.000760 |

1.028055 |

| 33 |

759.862 |

6 |

7 |

130 |

0.000221 |

-0.152693 |

-0.000047 |

0.006798 |

-0.030006 |

1.049221 |

| 117 |

624.538 |

20 |

5 |

150 |

0.000026 |

-0.133886 |

-0.000033 |

0.000090 |

-0.001823 |

1.024796 |

| 93 |

268.598 |

1 |

7 |

140 |

0.020558 |

1.247608 |

-0.000445 |

-0.065233 |

0.357433 |

1.027779 |

| 64 |

391.749 |

22 |

9 |

200 |

0.001846 |

0.489364 |

-0.000243 |

-0.012459 |

0.100476 |

1.039201 |

영향력이 큰 사례

cook distance가 큰 순서대로 정렬

- 4/표본수 이상이면 영향력이 크다고 할 수 있음.

1

2

|

album.resid_std = np.abs(album.resid_std)

album.sort_values(by = ['cook','resid_std'],ascending=[False, False])

|

|

adverts |

airplay |

attract |

sales |

cook |

resid_std |

dfbeta_adverts |

dfbeta_airplay |

dfbeta_attract |

covariance |

| 168 |

145.585 |

42 |

8 |

360 |

0.075704 |

3.067079 |

-0.002579 |

0.071664 |

0.107867 |

0.857218 |

| 0 |

10.256 |

43 |

10 |

330 |

0.065682 |

2.262619 |

-0.002828 |

0.025215 |

0.302940 |

0.953043 |

| 118 |

912.349 |

57 |

6 |

230 |

0.053361 |

1.709781 |

-0.000618 |

-0.111819 |

0.430083 |

1.013622 |

| 99 |

1000.000 |

5 |

7 |

250 |

0.050402 |

2.064131 |

0.001338 |

-0.098943 |

0.371103 |

0.967650 |

| 54 |

1542.329 |

33 |

8 |

190 |

0.050391 |

2.267631 |

-0.002619 |

0.004308 |

0.094568 |

0.944246 |

| ... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

... |

| 79 |

15.313 |

22 |

5 |

110 |

0.000026 |

0.092506 |

0.000056 |

-0.000595 |

-0.005664 |

1.029915 |

| 117 |

624.538 |

20 |

5 |

150 |

0.000026 |

0.133886 |

-0.000033 |

0.000090 |

-0.001823 |

1.024796 |

| 179 |

26.598 |

47 |

8 |

220 |

0.000025 |

0.045893 |

0.000048 |

-0.001569 |

-0.000459 |

1.056691 |

| 141 |

893.355 |

26 |

6 |

210 |

0.000023 |

0.089516 |

0.000044 |

0.000217 |

-0.001188 |

1.029495 |

| 109 |

102.568 |

22 |

7 |

140 |

0.000013 |

0.050878 |

-0.000035 |

-0.000455 |

0.007294 |

1.036476 |

데이터 출처 : SpringSchool